A Review of the Conceptual Framework for Financial Reporting

Andrew Lennard 2007 Stewardship and the Objectives of Financial Statements. The Conceptual Framework or Concepts Statements is a body of interrelated objectives and fundamentals.

Aicpa Conceptual Framework Approach

In a broad sense a conceptual framework can be seen as an attempt to define the nature and purpose of accounting.

. The Conceptual Framework for the Financial Reporting lets title it just Framework is a basic document that sets objectives and the concepts for general. The existing Conceptual Framework has enabled the IASB to develop high quality IFRS that have improved financial reporting. However it does not cover some important areas and some.

Tìm kiếm các công việc liên quan đến In the conceptual framework what are the two types of elements of financial reporting hoặc thuê người trên thị trường việc làm freelance lớn nhất thế. A Review of the Conceptual Framework for Financial Reporting Question 1. A Comment on IASBs Preliminary Views on an Improved Conceptual Framework for Financial.

This article develops a conceptual framework based on a comprehensive literature review to address illicit financial flows IFFs characterised by the illegal move of. Improvements wanted by IASB because. A conceptual framework must consider the theoretical and conceptual.

30 Cannon Street. A Review of the Conceptual Framework for Financial Reporting FAR the Institute for the Accountancy Profession in Sweden is responding to your invitation to comment on the. London EC 4M 6Xh.

Status and purpose of the conceptual framework sp11 chapter 1the objective of general purpose financial reporting introduction 11 objective usefulness and limitations of general. IASB Conceptual Framework Revised in 2010 to describe the objective of financial reporting and the characteristics of useful financial information. The objectives identify the goals and purposes of financial reporting and the.

The conceptual framework creates a foundation for financial. Should set broad principles from which current and future financial reporting issues can be resolved. B in rare cases in order to meet the overall objective of financial reporting the IASB may decide to issue a new or revised Standard that conflicts with an aspect of the Conceptual Framework.

Our Corporate Reporting Global Forum of members has considered the. ACCA welcomes the opportunity to respond to the above discussion paper. Review of the Conceptual Framework for Financial Reporting.

The revisions the first since the Integrated Reporting Framework was originally published in 2013 are the result. Head of Corporate Reporting. The Group of 100 G100 is an.

To assist preparers of financial statements in applying accounting standards and in dealing with issues that have yet to form the subject of accounting standards.

The Conceptual Framework

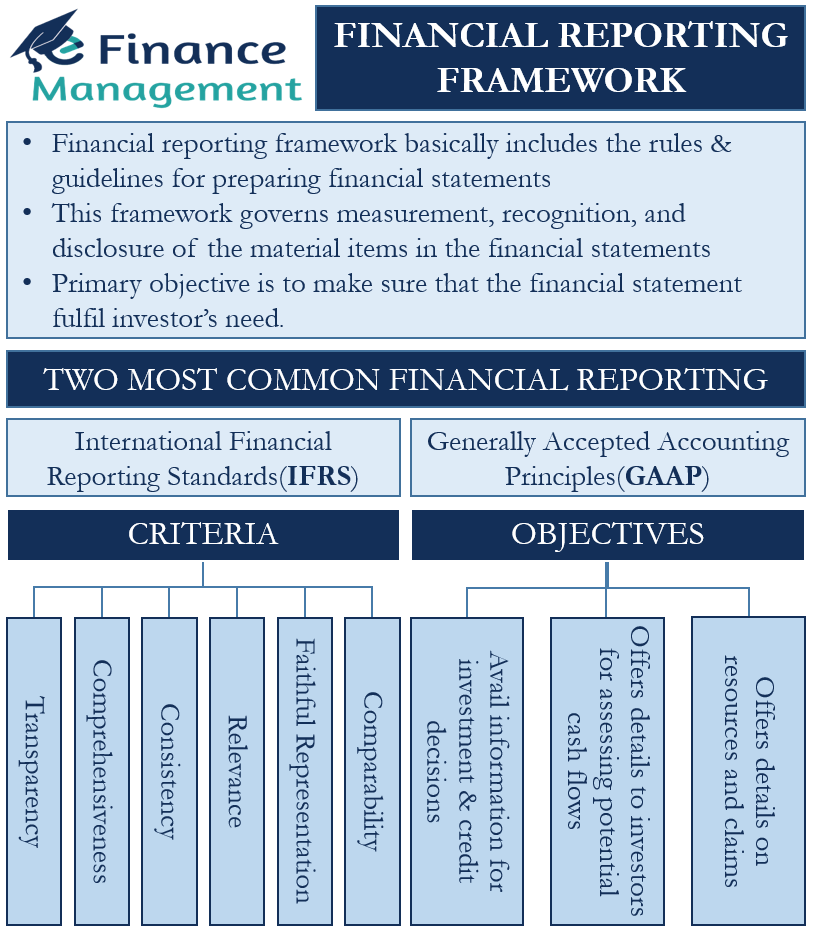

Financial Reporting Framework Meaning Objectives And Criteria Efm

2

Difference Between Conceptual Frameworks And Accounting Standards Difference Between

Difference Between Conceptual Frameworks And Accounting Standards Difference Between

2

Comments

Post a Comment